Debt…

Almost everyone is in it…

And almost everyone dreams of winning the lottery to get out of it.

(There’s no logical reason for this photo. I just Googled debt meme and came up with it.

A squirrel… in full armor.

You’re welcome.)

So we worked hard, and became debt free.

We cut up all the credit cards, and paid them off. We paid off the cars, motorcycles and other assorted big boy toys.

Three months ago? We paid off our mortgage.

We’re now totally debt free.

Yay us!

Except no. Life doesn’t work that way.

For years we had nearly perfect credit scores.

(Perfect is 840, ours was 837.)

Until we started paying off debt, at which point they dropped like a stone.

Cut up and pay off your credit cards? Lose 34 points.

Which is wrong. So very, very wrong.

In every conceivable way.

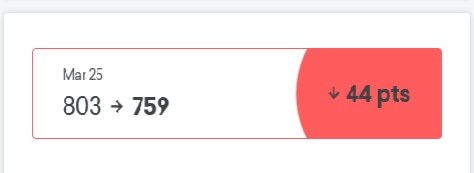

The last time I checked?

It went down 44 points because we no longer have a mortgage.

What the f*ckity f*ck f*ck?

Everything we own is paid for, we have more liquid cash than we’ve ever had before, our pension and retirement plans are set and we can live comfortably without fear.

For this we’re penalized?

It is.

It really, really is.

so you dont want debt but perfect credit score? for what? 🙂

LikeLiked by 1 person

Who doesn’t want perfection? And besides, it ticks me off they penalize you for managing your money correctly.

LikeLiked by 2 people

That sucks. The husband and I are very competitive with each other over our individual credit scores. Suddenly our mortgage doesn’t seem so onerous.

LikeLiked by 1 person

It really does suck. Isn’t being debt free what we all strive for? Burning the mortgage papers used to be cause for celebration… now you have to take out another loan to retain stays quo. It’s just wrong.

LikeLiked by 2 people

I’m sure you realize that our economic system is based pretty heavily on most people being in debt that they can never pay off. It isn’t sustainable, of course, but no one in charge seems to look further than five years down the road…

LikeLiked by 1 person

It’s evil is what it is. Predatory lending, and charge, charge, charge. Can’t afford it? Who cares. We’ll reward those who are drowning in debt.

Evil.

LikeLiked by 1 person

Evil? Maybe it is just a horrible and malicious idea that everyone mistakes for evil…

LikeLiked by 1 person

I had a girlfriend in NC whose husband worked for a cable company. They applied for a mortgage to buy a house they couldn’t afford. The company encouraged them to inflate their combined income to qualify. They got the house…. and lost it 4 years later because they couldn’t make the payments. Sorry, but that’s evil enough for me.

LikeLiked by 1 person

Yep. Makes no sense but financial institutions play games. They only like you if they think there’s a way to get more money out of you. Once that mortgage is paid off, you’re no longer a potential player in their game.

LikeLiked by 1 person

Well, it feels great not to have to play anymore. It’s amazing how much money you actually find in your paycheck when those monthly payments are gone. Still pisses me off about the scores though.

LikeLiked by 1 person

When I bought my home ten years ago (Yes, I’m only a third of the way through my mortgage), I had no credit. Zero. I was very lucky to find someone who would give me a mortgage because, as I was told time and time again, having no credit is actually WORSE than having bad credit. I never have and never will understand that philosophy, but then again, I’m not a lender…. of money or things.

My favorite part of the process was the “credit classes” I had to take before I could get approved. I was taught to put a tank of gas on credit and make the minimum payments on it until it was paid off…. rinse, wash, repeat. Uhhhhh, no. I pay off my balance each month and could care less what my score says…

LikeLiked by 1 person

Exactly. They want you to carry a balance… they want you to be in debt because big corporations make money on the interest you pay. Late on one credit card payment? The interest on ALL your cards goes up. Tell me that’s not evil.

LikeLike

sheesh!

LikeLike

I’m not proud about what I’m about to say but…..I am a bankruptcy survivor for the exact same reasons as 80% of the country that’s in debt. So you pay off everything and you credit score goes down, that is pure bullshit! But, when you have no credit score and need to build it up, you can’t unless you go into debt with said credit card. Then the “financial counseling” your forced to take when you begin bankruptcy say’s you should use a credit card for food and gas, and pay off everything BUT leave 10% of the balance on the card. This is so that the credit card companies or anyone that pulls your credit report sees you have an open credit line. I have lived five entire years without a credit card because of bankruptcy, but now I want to buy a house and I need to build up my credit score in order to do so, but I can’t unless I go out and FUCKING buy something on credit! I agree with evilsquirrel13 (cool name by the way) paying off the credit card each month is the best way to go. But either way, you pay off your debt or you have too much debt on your credit report, it’s going to fuck over the numbers for you no matter how good you are at taking care of it.

LikeLiked by 1 person

The thing that really bugs me is they encourage debt. No debt? No credit. Forget that we have 35 years worth of paying off debt on time and in full. If that’s not history, what is?

I understand the bankruptcy dilemma, it’s a crazy Catch 22… and also wrong.

LikeLiked by 1 person

The term credit card companies use for the people who pay off their debt at the end of every month is: deadbeat.

LikeLiked by 2 people

You don’t want to hear my term for credit card companies….

😠

LikeLiked by 1 person

Well, it’s awesome that you’ve paid off all your debt. Congratulations! We paid off our home last year, but we have two car payments. Blah! Damn cars.

LikeLiked by 1 person

I paid off my last new one in 2 years, that was a killer. But at least now it won’t break down as soon as it has a clear title!

LikeLiked by 1 person

Wow, how rude! There’s no reason you should be penalized for being debt free. But a huge congrats to actually being debt free! I’ve never known anyone like you in real life,lol, I though debt free people were like unicorns… they only exist in fairy tales.

LikeLiked by 1 person

It wasn’t easy. The system really is stacked against us unicorns…

😉

LikeLiked by 1 person

I have a score of 823–want to know how?? Be old & poor, have nothing in the bank (or under the mattress)–have 6 credit cards and charge your food bills on each and pay them at the end of the month–after you do that I’ll tell you the rest! Oh yes –before the above declare bankruptcy twice!

LikeLiked by 1 person

Nice.

Except for the poor and having nothing and bankruptcy part….

😉

LikeLike

It didn’t used to be this way. My dad used to talk about how he got a store credit card back in, I’d guess, the 50s and he’d purchase something and immediately pay it off and that’s how he developed good credit. I think it all changed with the credit reporting agencies, which I’ve heard shady things about a couple years ago.

I’m sure there are workarounds to not having a credit score or not having a good one. I’ve heard a lot of people recommend Dave Ram

LikeLiked by 1 person

Ugh! Dave Ramsey. Stupid no edit comment feature on wordpress!

LikeLiked by 1 person

Dave Ramsey?

LikeLiked by 1 person

True. Back in the day being able to manage your money and be debt free was actually a good thing.

LikeLiked by 1 person

I have eight years before my mortgage is paid off, my car… is in 5 months.

I want the debt gone (and it is going) but it s*cks what happens to the “good” credit rating. 😦

LikeLiked by 1 person

It’s wonderful being debt free, I highly recommend it. But if I had it to do over again I would keep one damn credit card and charge occasionally.

LikeLike

Honestly; the real winner in this game is the one who doesn’t play.

LikeLiked by 1 person

Yeah. It’s pretty screwy. And did you know that having/using debt just under half your revolving limit is ideal? So if you have a charge card with a $3000 limit, you’re better off maintaining about a $1000 balance? Because see, they’re looking to keep you paying, the creditors, the credit bureau.

Also, remember, unless you need to get new credit, the credit score doesn’t even matter. Being debt free is absolutely fantastic and above 700 you’re still a fantastic mark — I mean, risk 😉

LikeLiked by 1 person

Yes, but it’s still wrong. And I’m sure there will come a day when we want a loan for something again… new car? Motorcycle? Boat? Who knows. The way things work they’ll probably charge us higher interest. Grrr.

🤢

LikeLike

No, above 700 you’re aces. Trust me. Best rates. Fall below 700, slight variations depending on the lender. It’s when you fall below 650 the pains come. Fall below 600 and almost no one will lend, and if they do, oh. my. gawwwwd. That won’t happen to you. It just won’t. It’s stupid and unfair, but it doesn’t matter — you’re debt free! Woot!

LikeLiked by 1 person

Thank you. I’ll take that pat on the back…. it was hard won.

😊

LikeLiked by 1 person